Silicon Valley Newsletter - June 2026

Real Estate

Real Estate

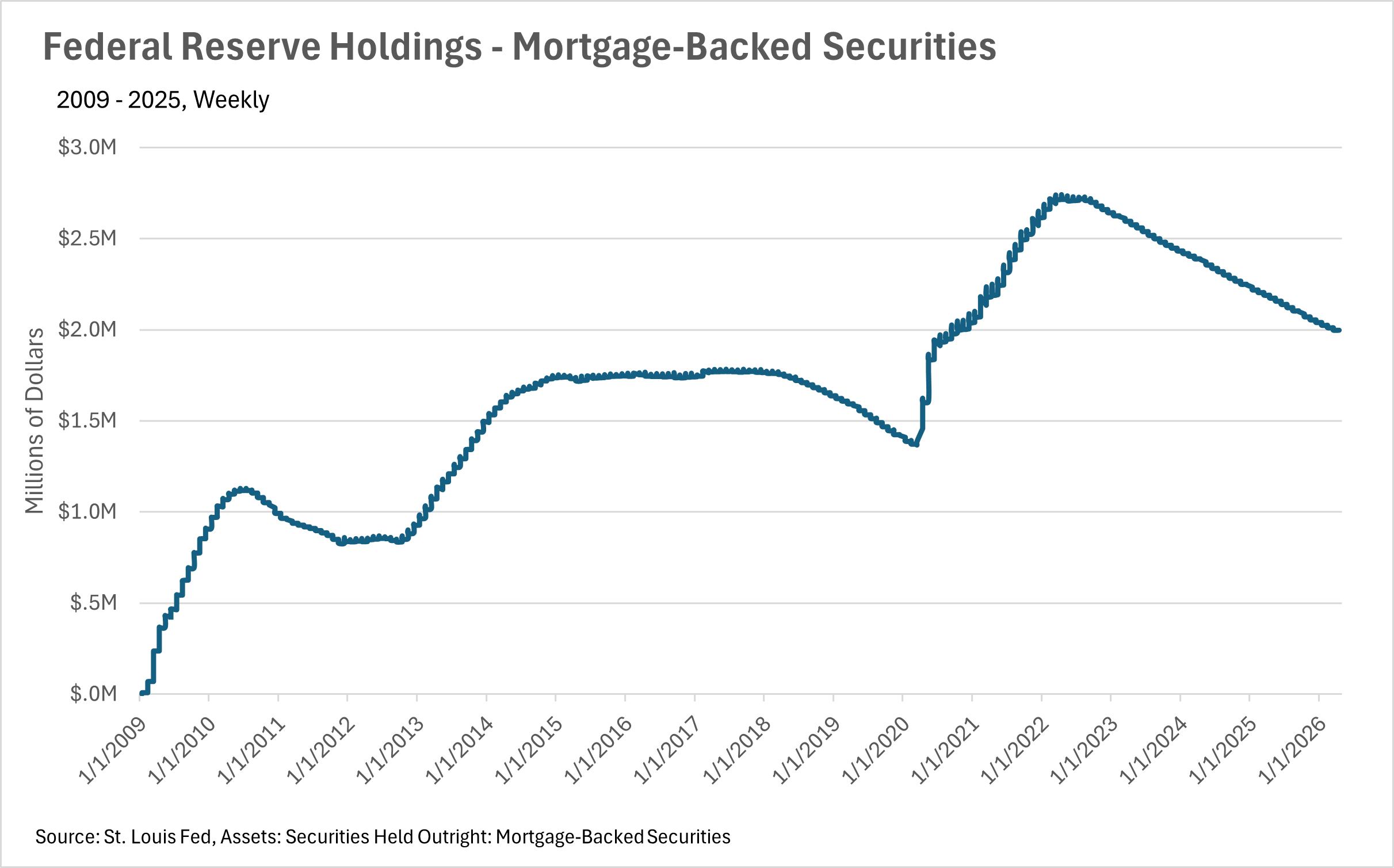

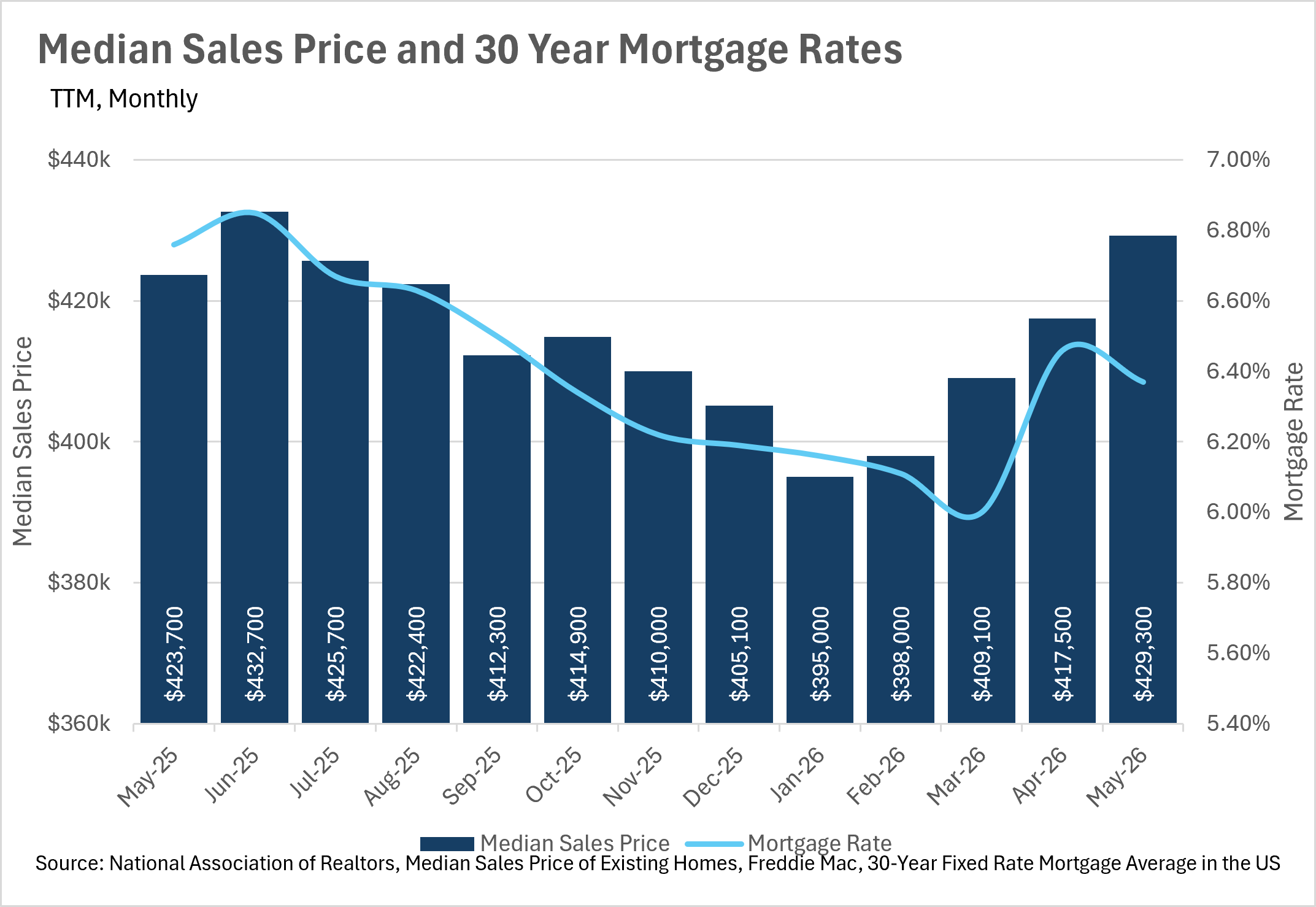

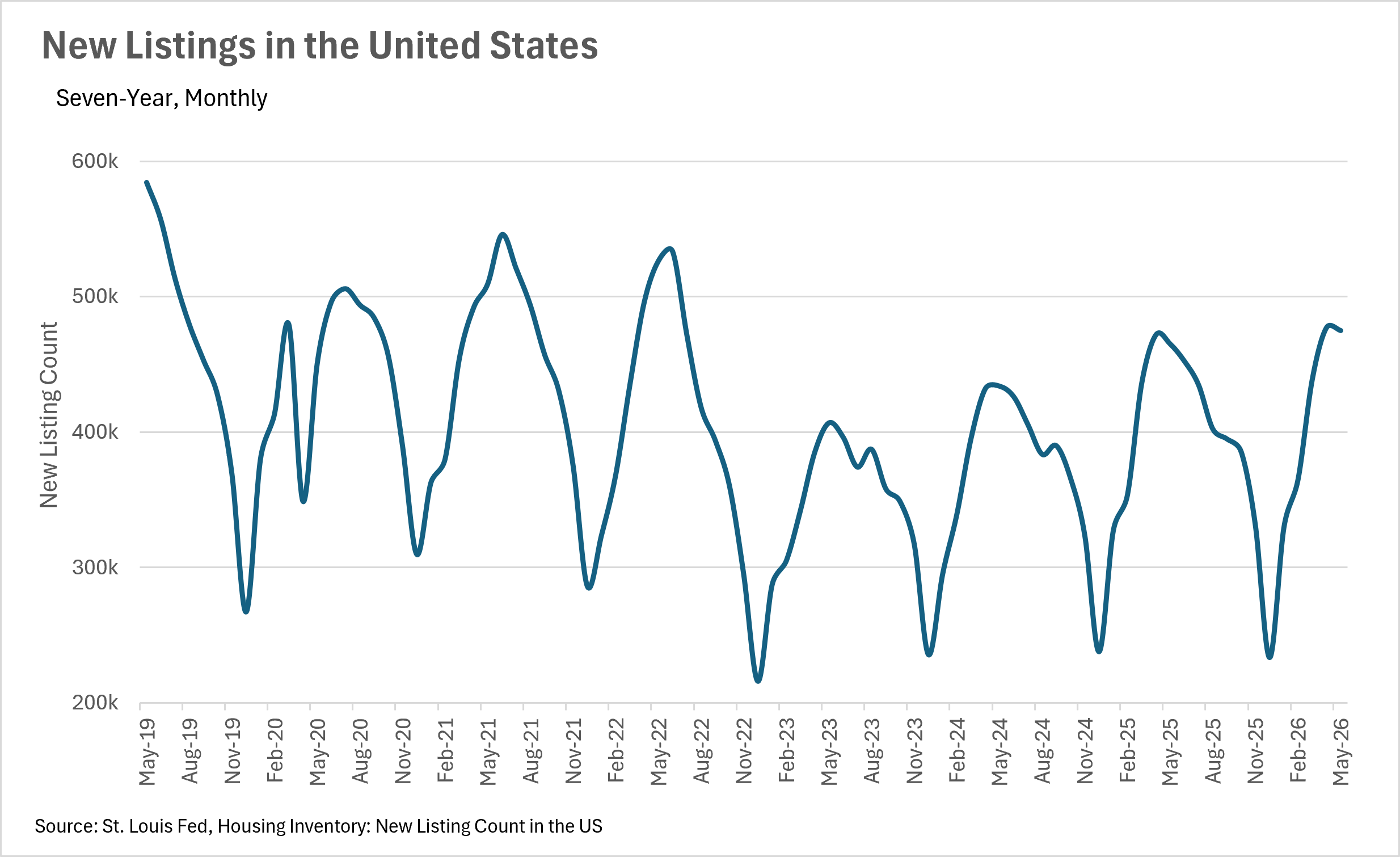

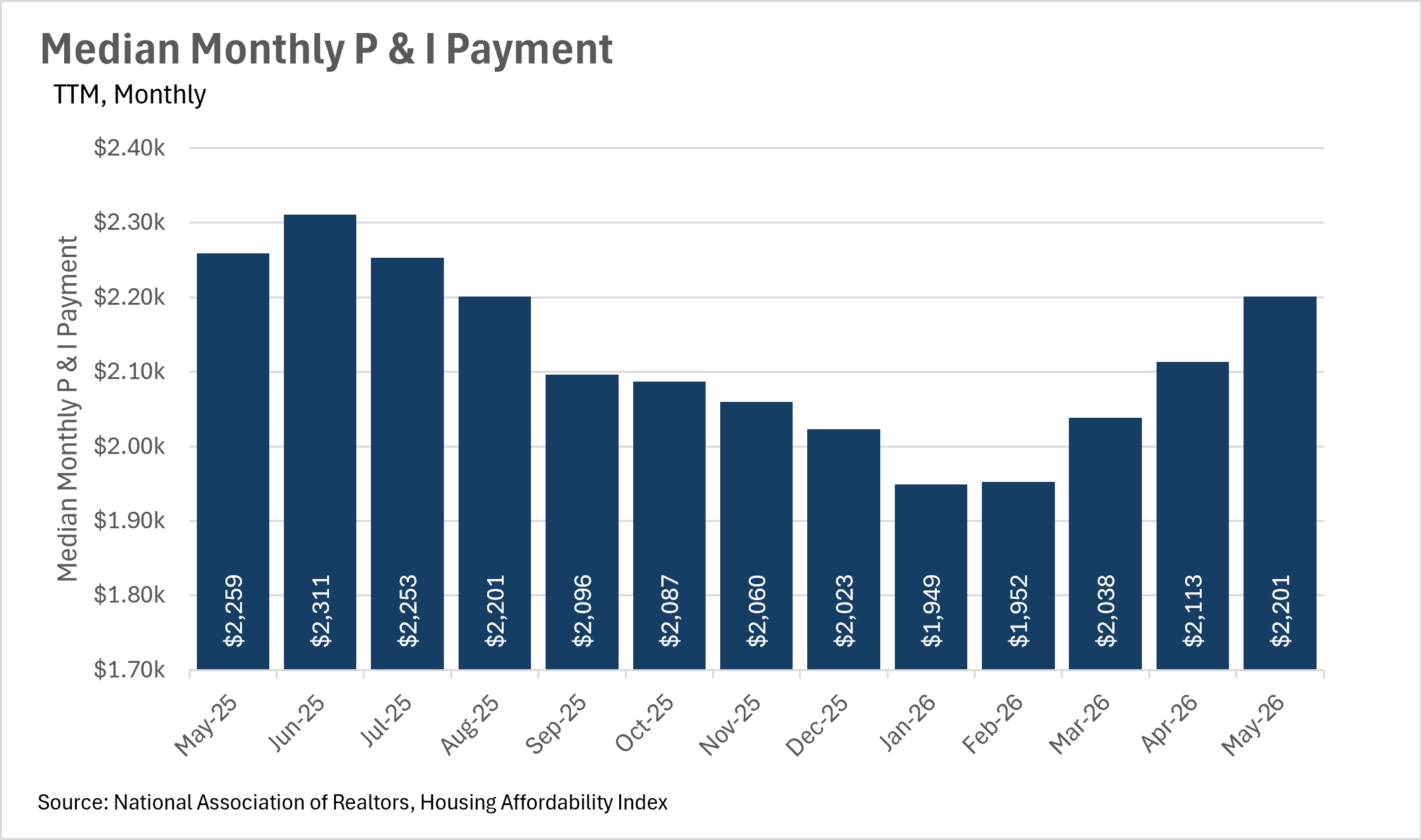

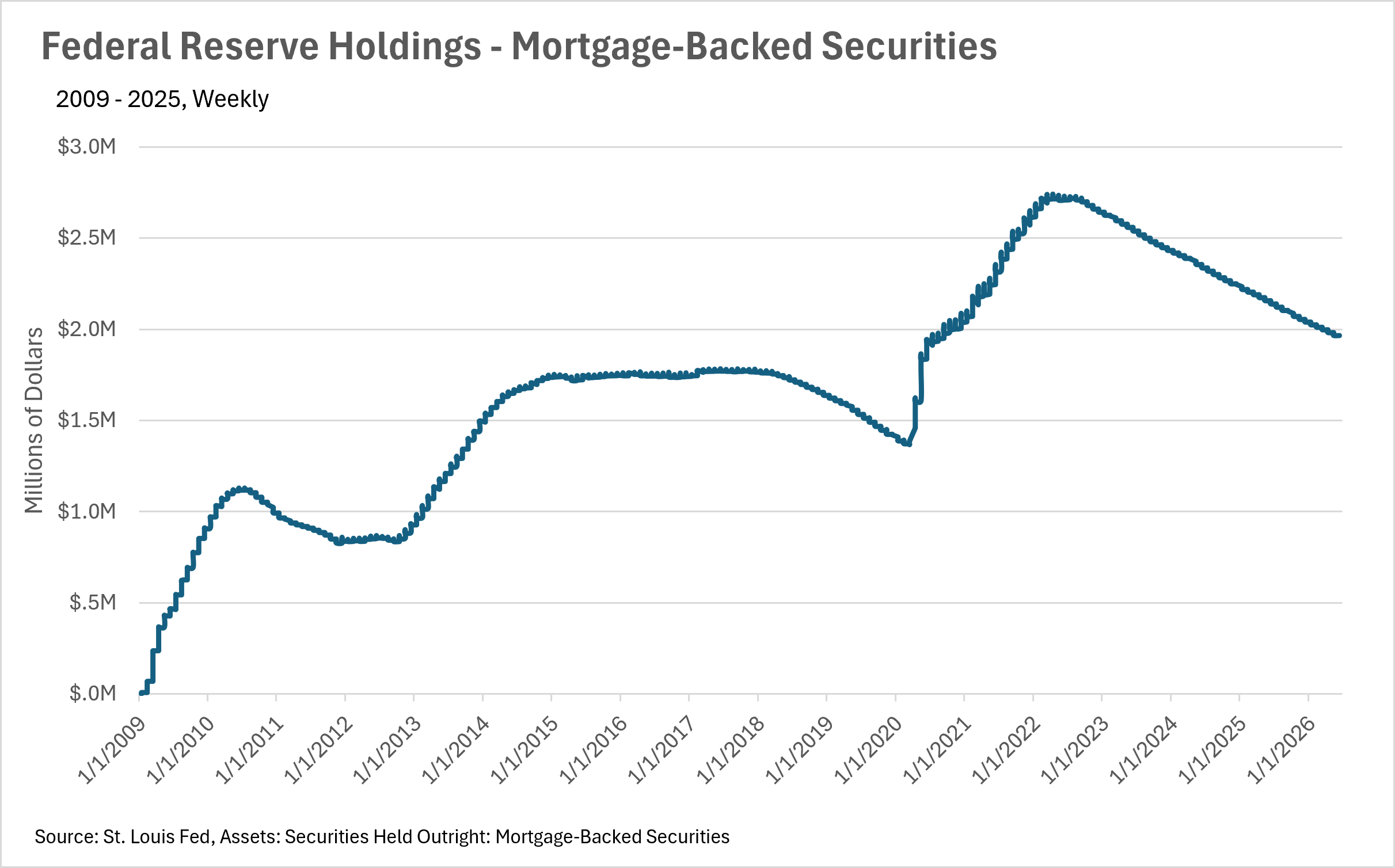

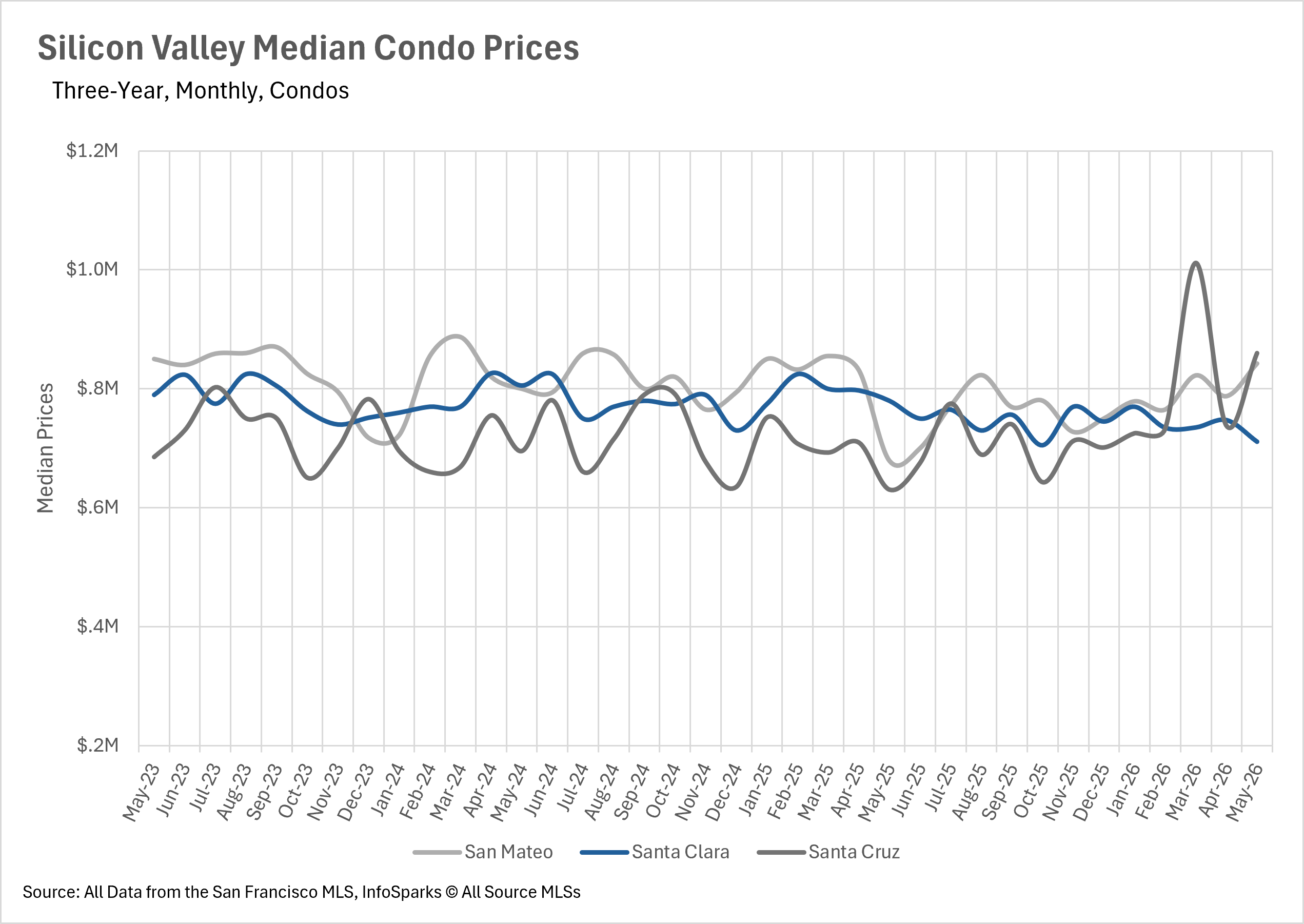

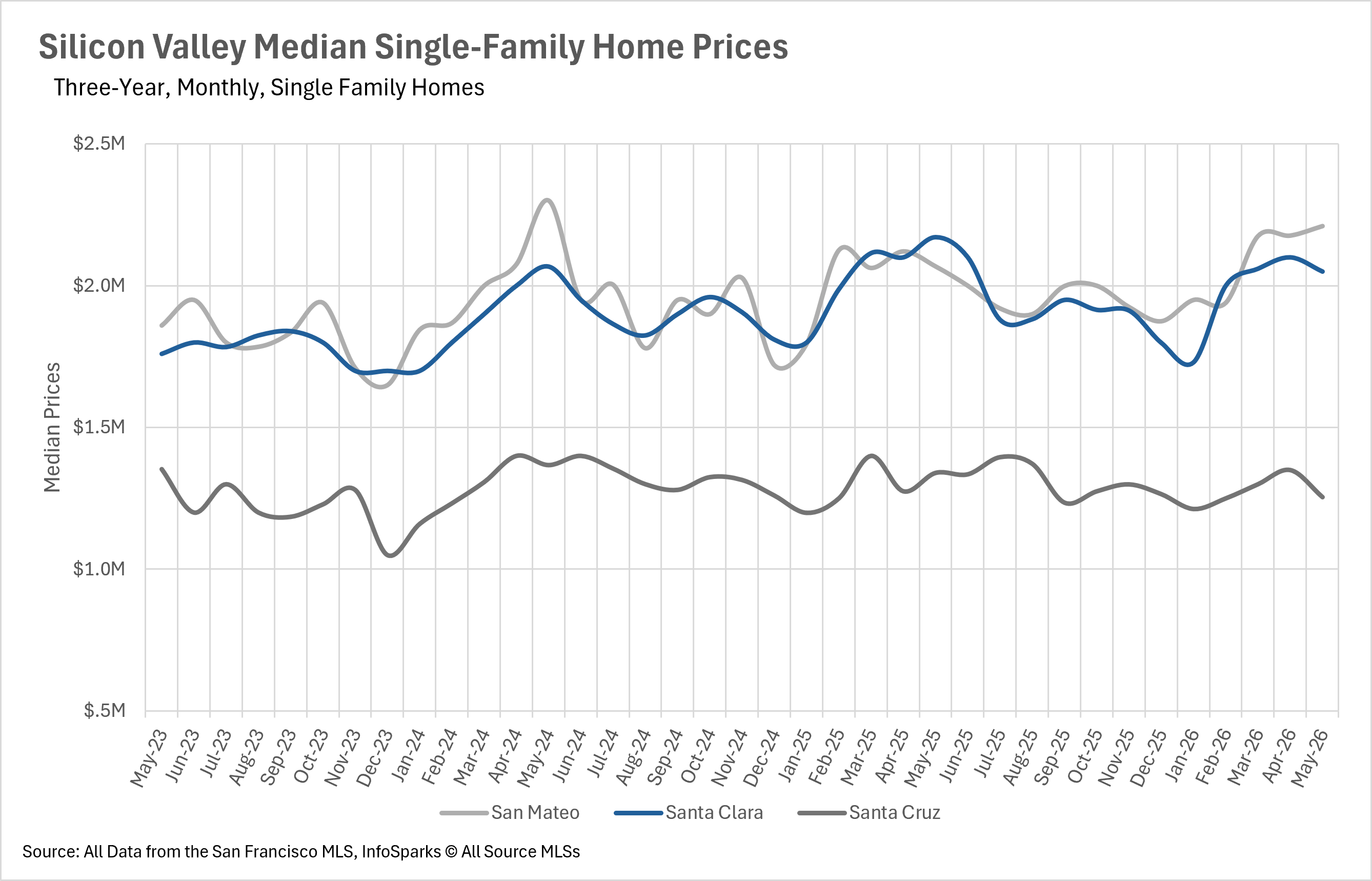

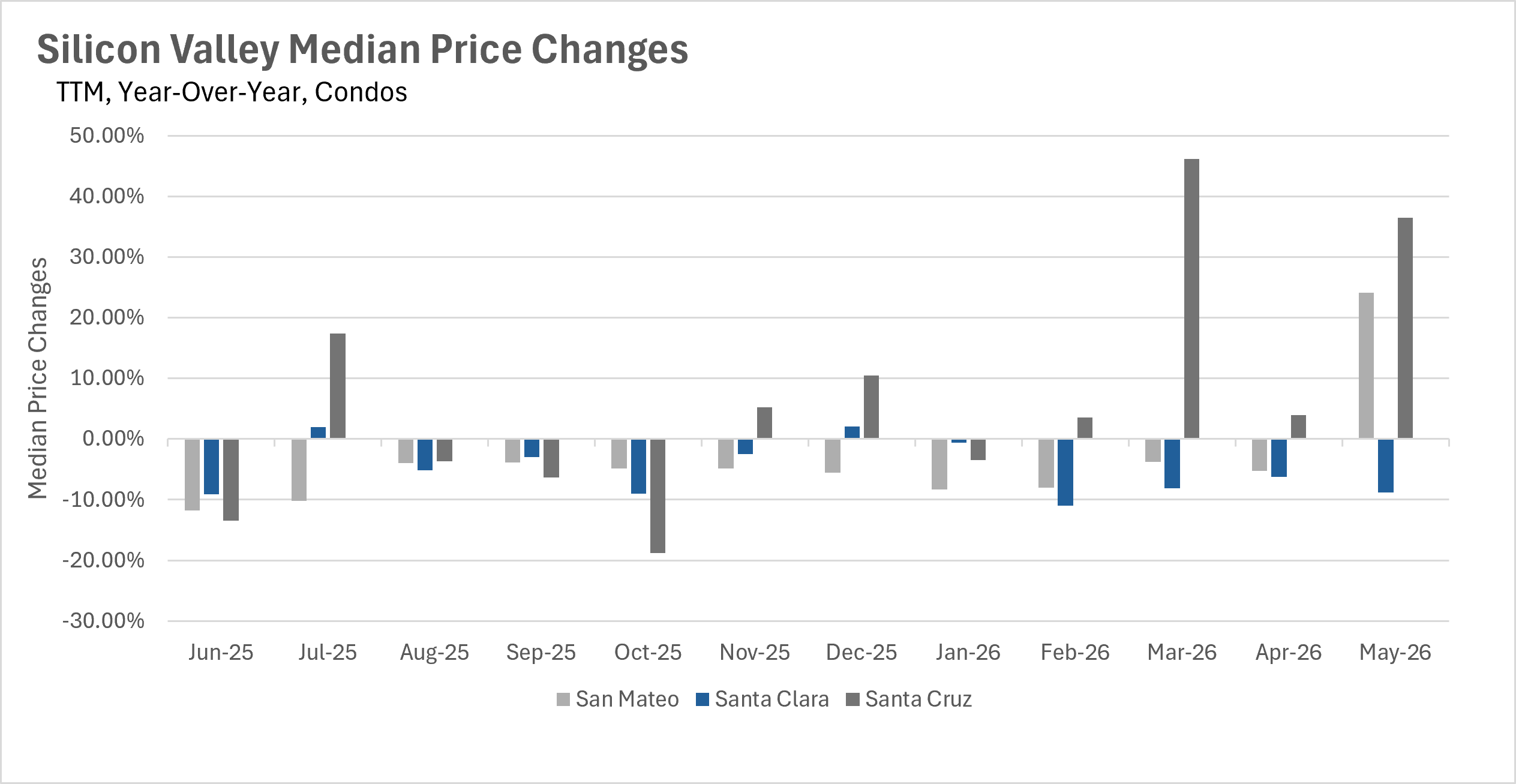

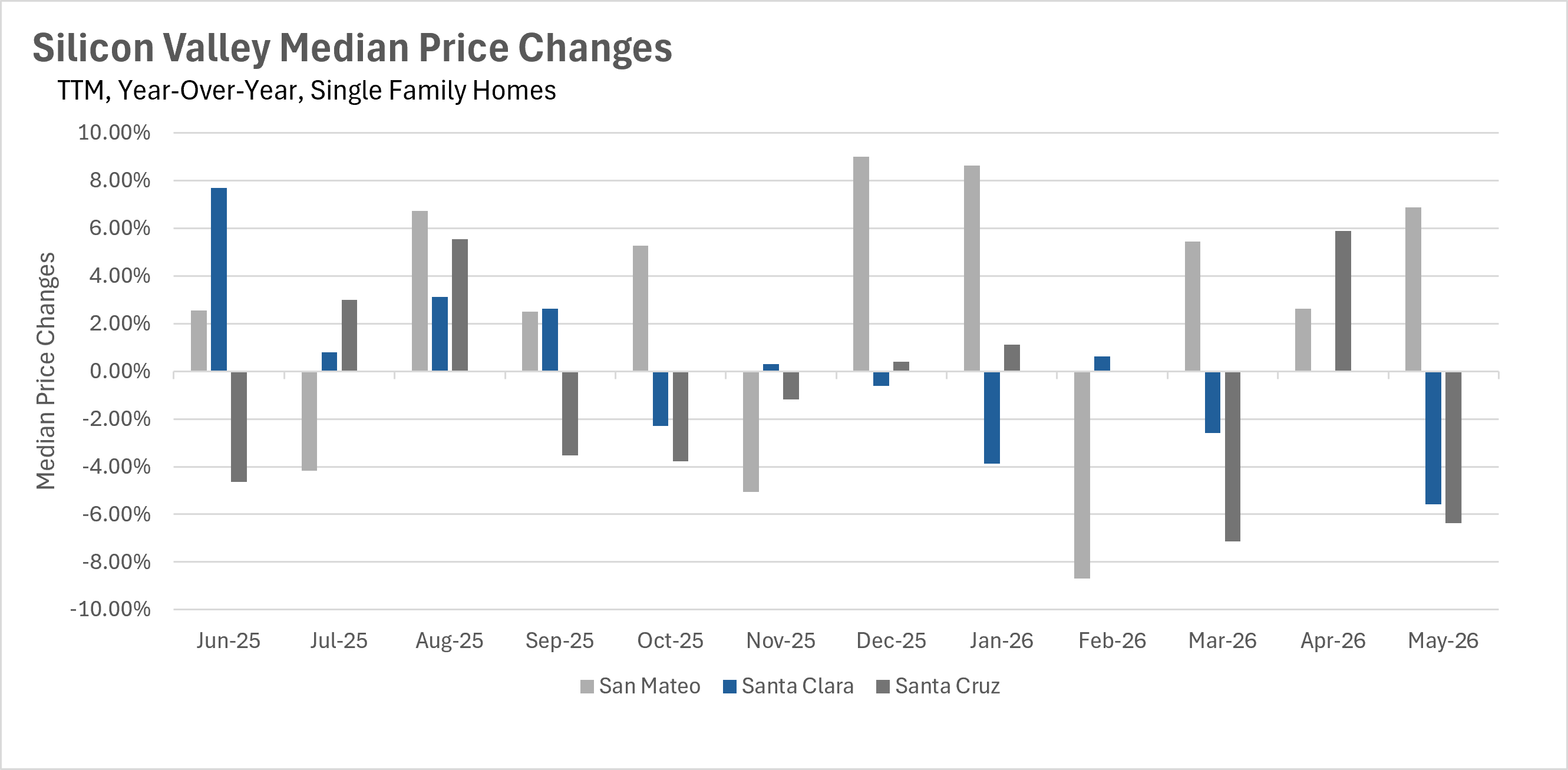

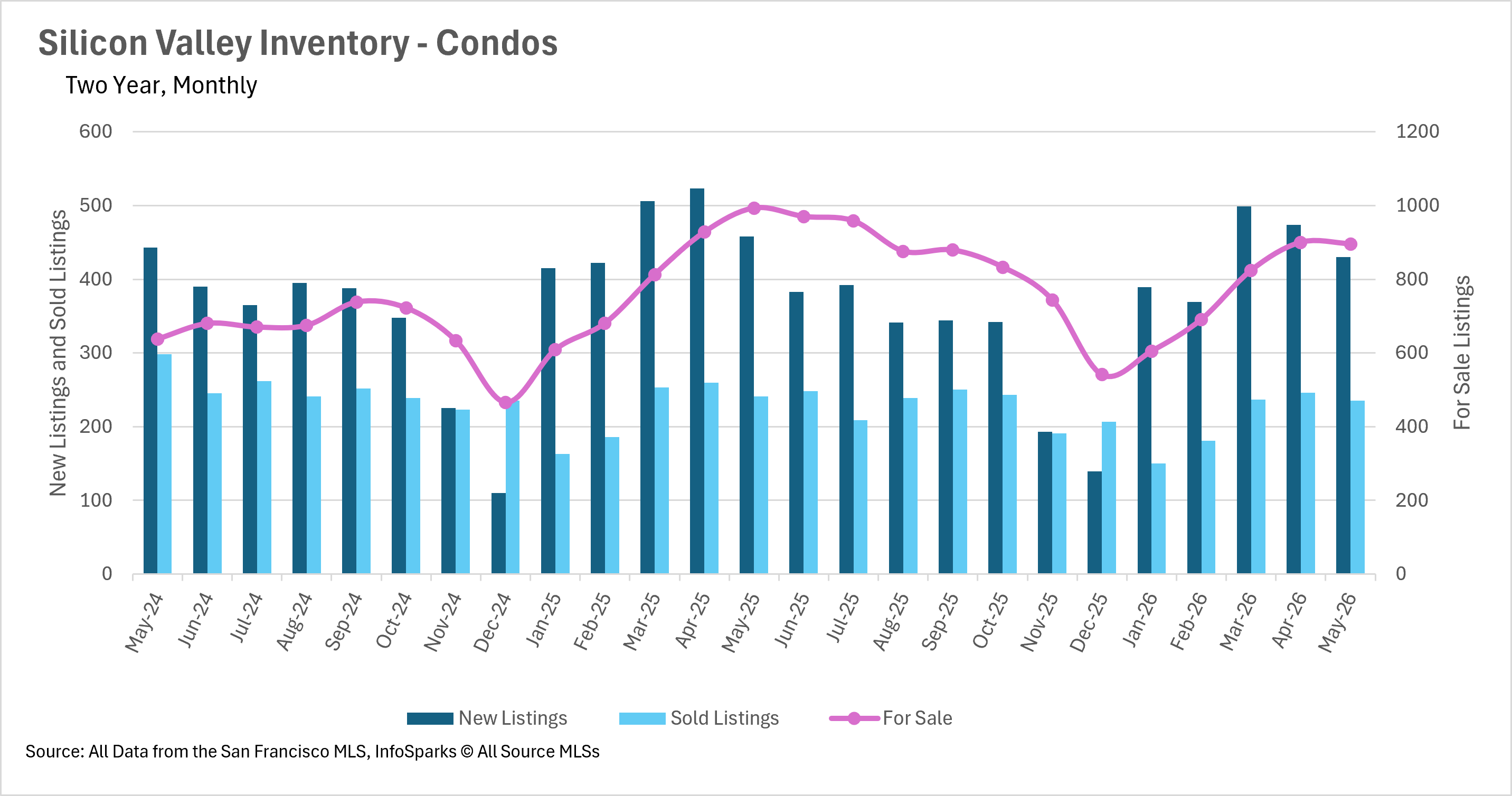

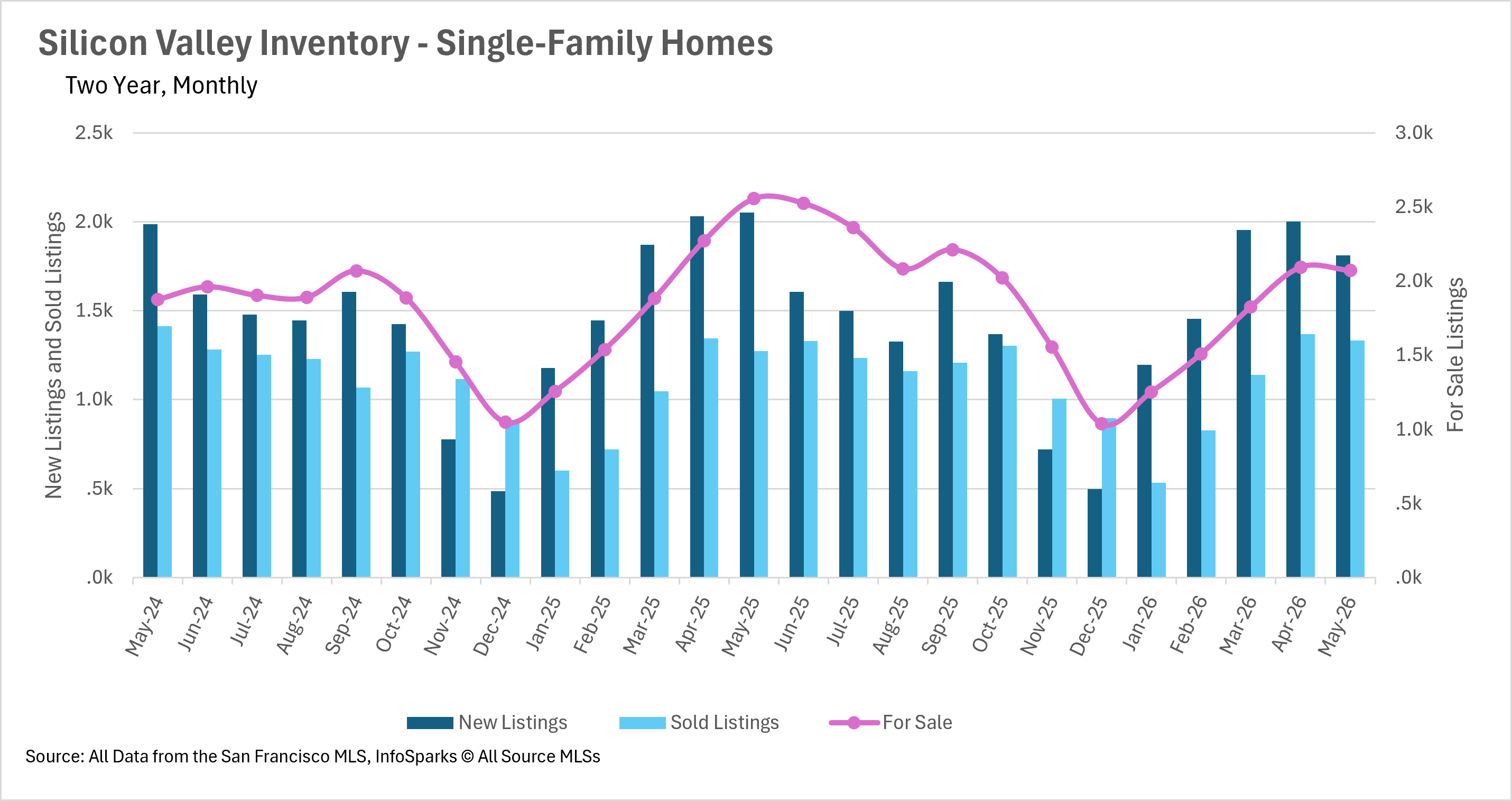

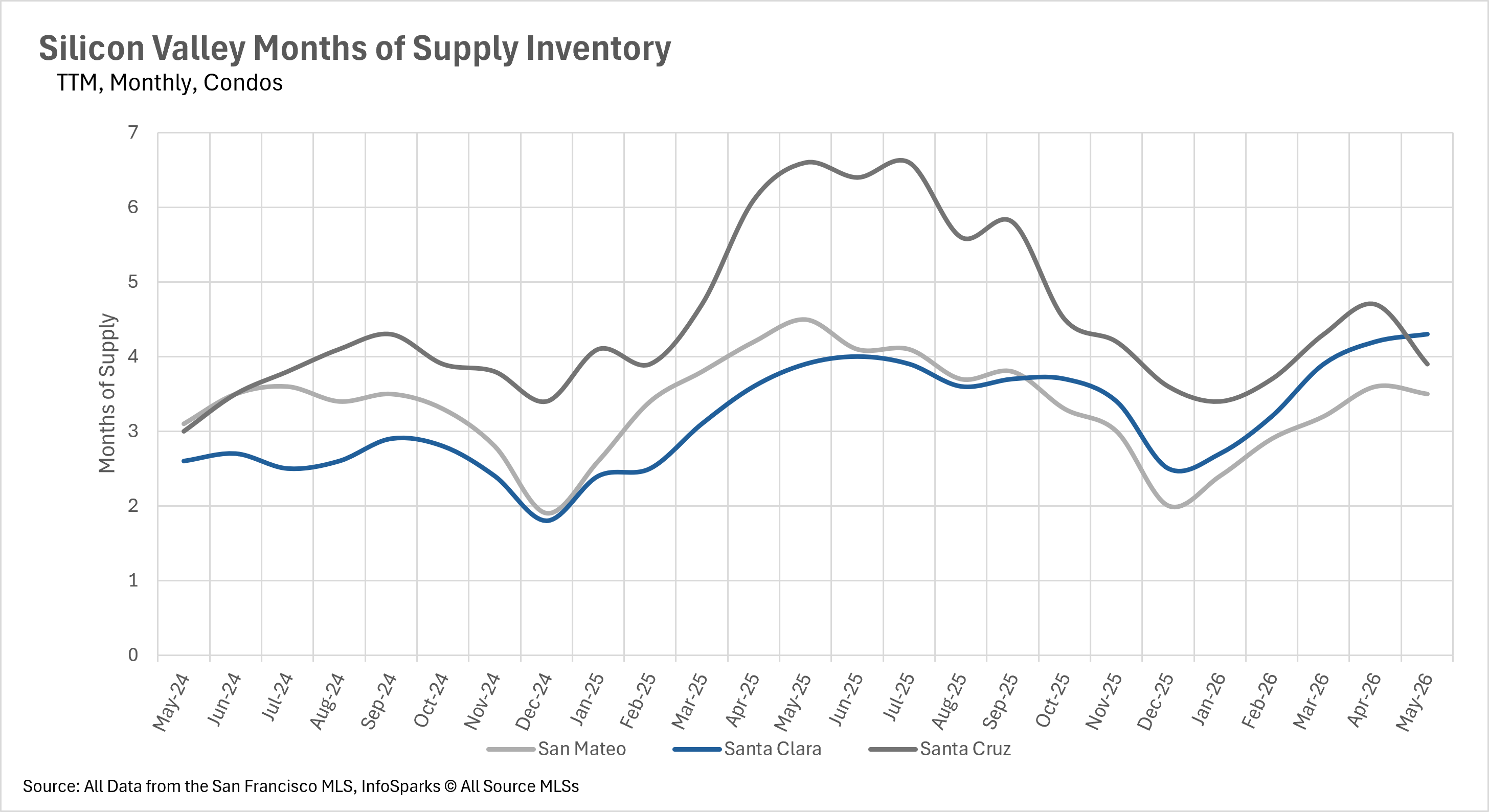

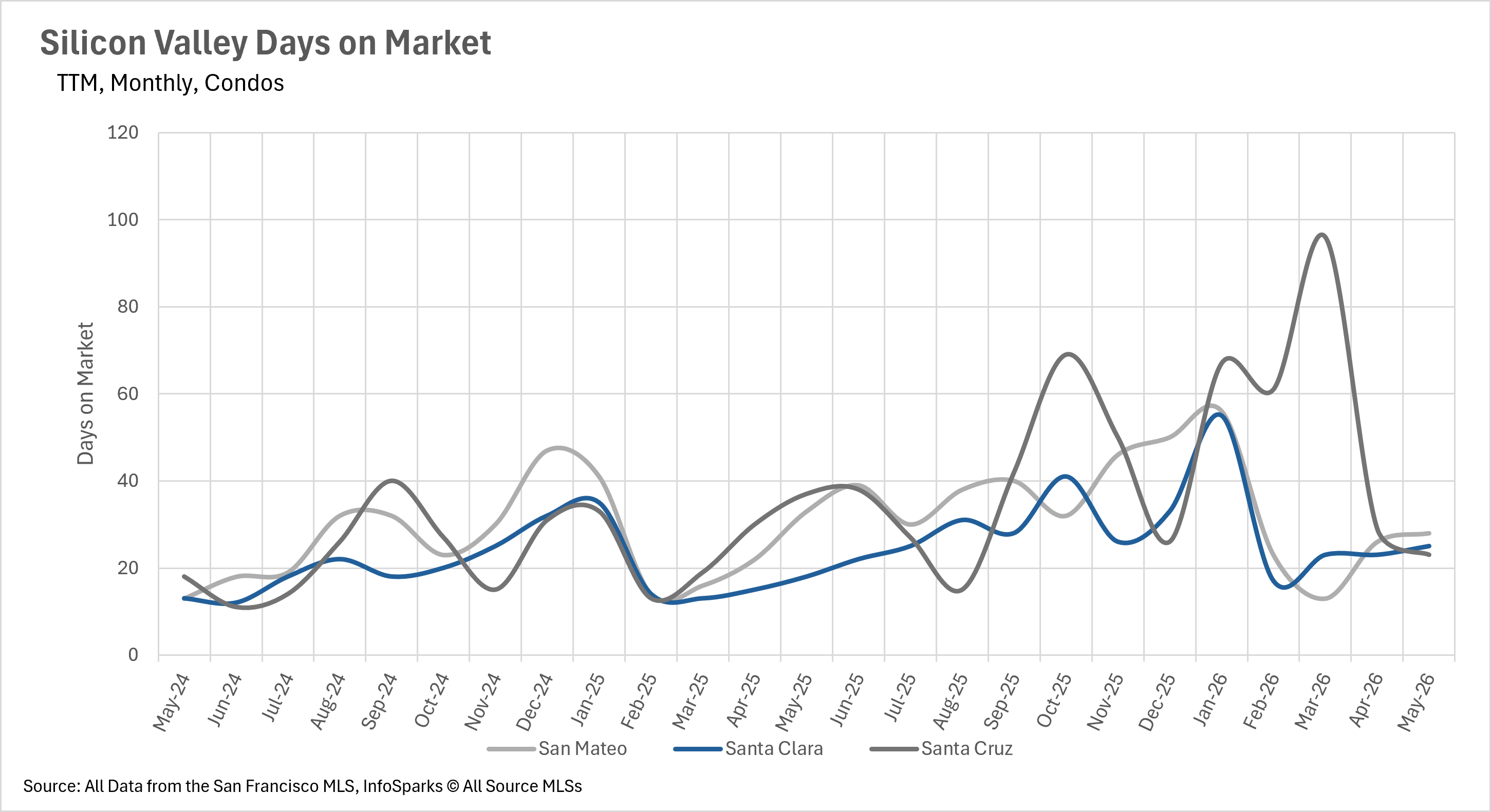

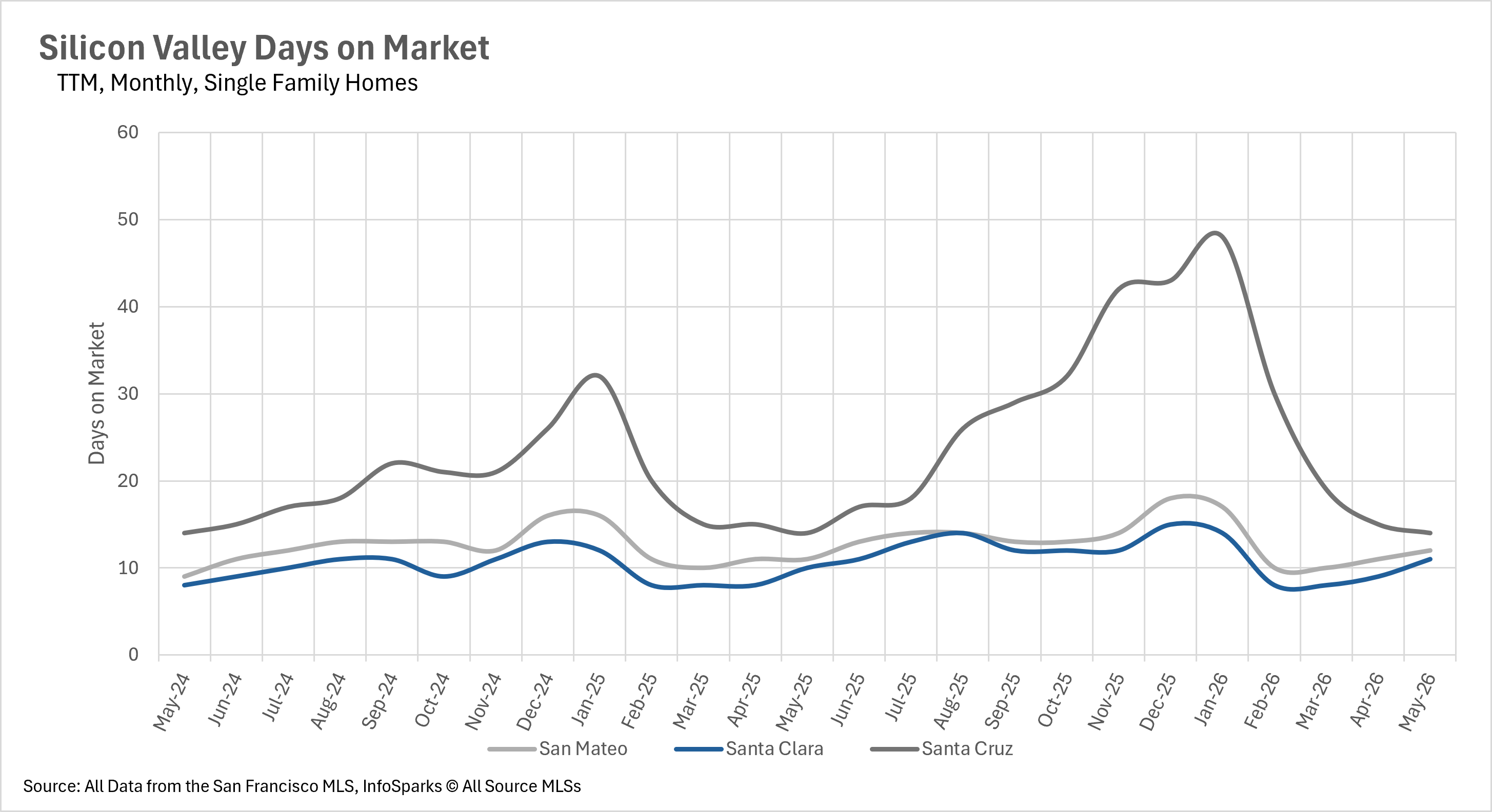

Note: You can find the charts & graphs for the Big Story at the end of the following section.

Single-family homes continue to sell quickly across the region, with the average listing spending just 11 to 14 days on the market.

Patrice and the Illuminate Properties team specialize in helping Palo Alto, Mountain View, Los Altos, Los Altos Hills, Menlo Park, Portola Valley, Redwood City, San Carlos, Sunnyvale, and Woodside buyers and sellers navigate today’s evolving market with confidence.

Stay up to date on the latest real estate trends.

Learn how water-smart landscaping can increase your Los Altos Hills home's value with drought-tolerant plants, smart irrigation, fire-wise design, and sustainable luxu… Read more

Discover how Sand Hill Road shapes Menlo Park home values. Learn how venture capital, luxury neighborhoods, buyer demand, and Silicon Valley drive real estate prices.

Explore the best outdoor activities in Menlo Park, CA. Discover parks, hiking trails, bike paths, swimming, golf, and recreation that make Menlo Park an ideal place to… Read more

Discover the fascinating history of Menlo Park’s tech industry, from the invention of the computer mouse and the birth of personal computing to Sand Hill Road venture … Read more

Explore the May 2026 Silicon Valley housing market update. Learn how rising home prices, increasing inventory, lower mortgage rates, and strong buyer demand are shapin… Read more

Discover the best outdoor activities in Los Altos Hills, CA. Explore Hidden Villa, scenic hiking trails, bird watching, photography spots, picnicking, and nature exper… Read more

You’ve got questions and we can’t wait to answer them.