Silicon Valley Newsletter - October 2025

Real Estate

Real Estate

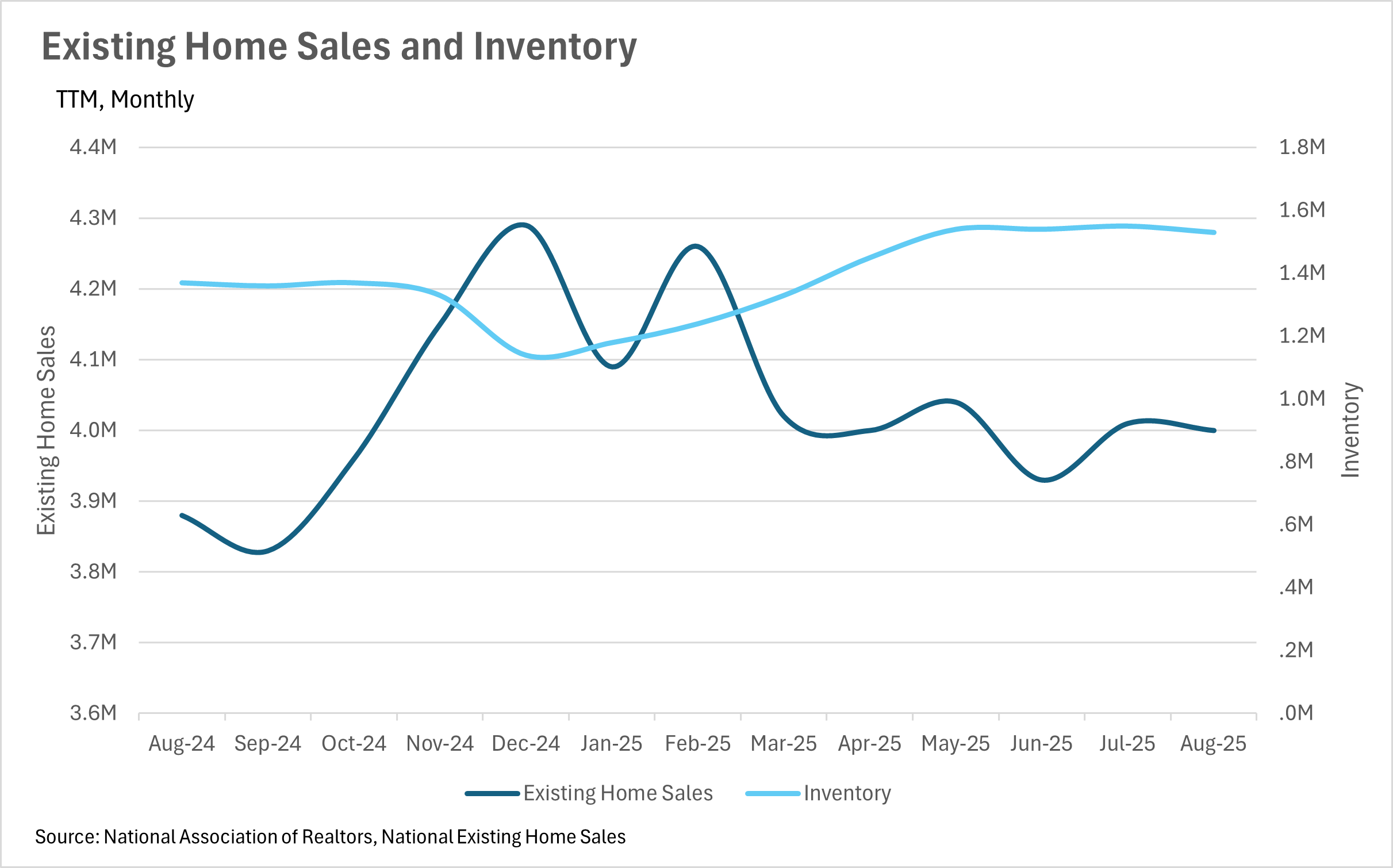

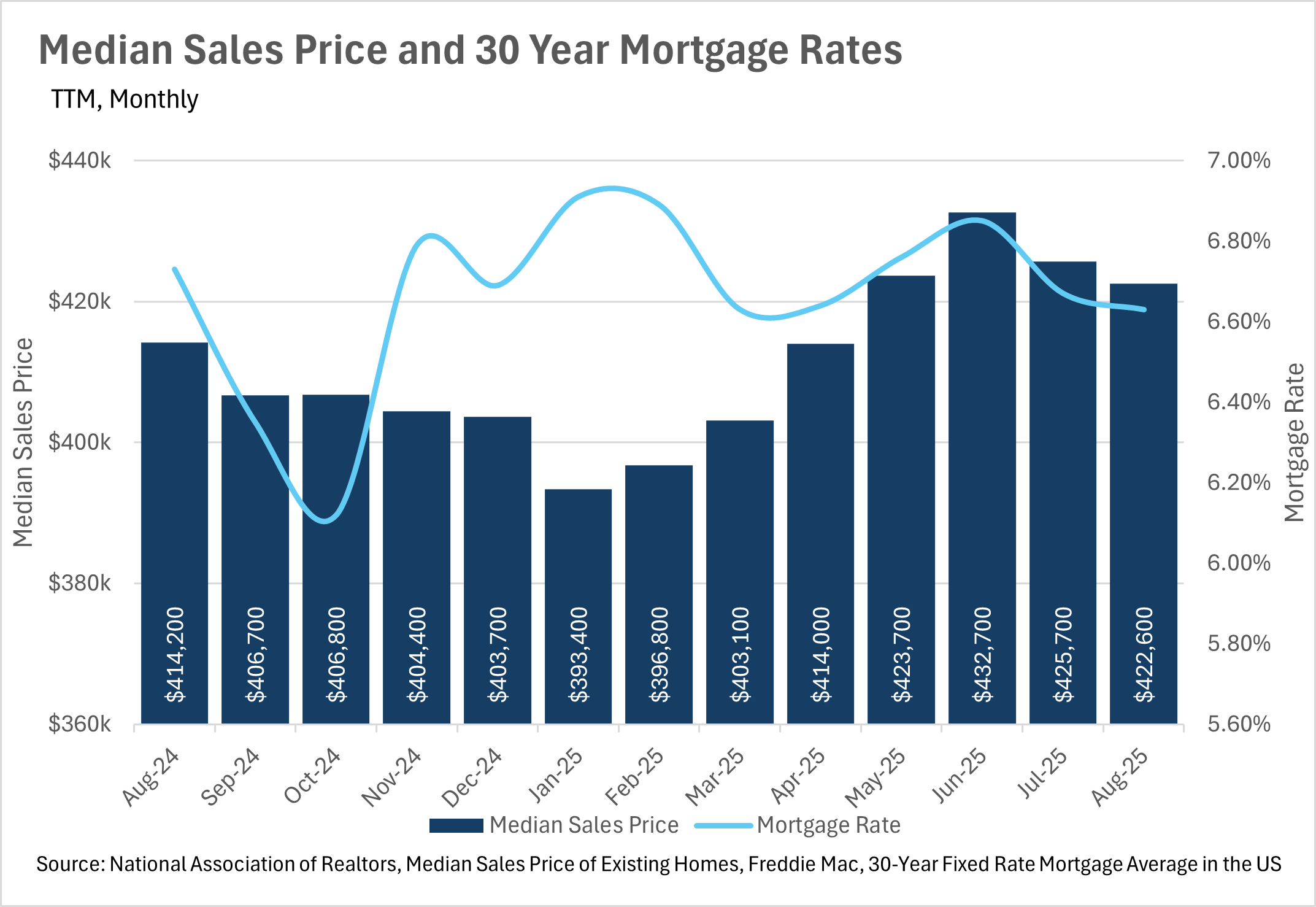

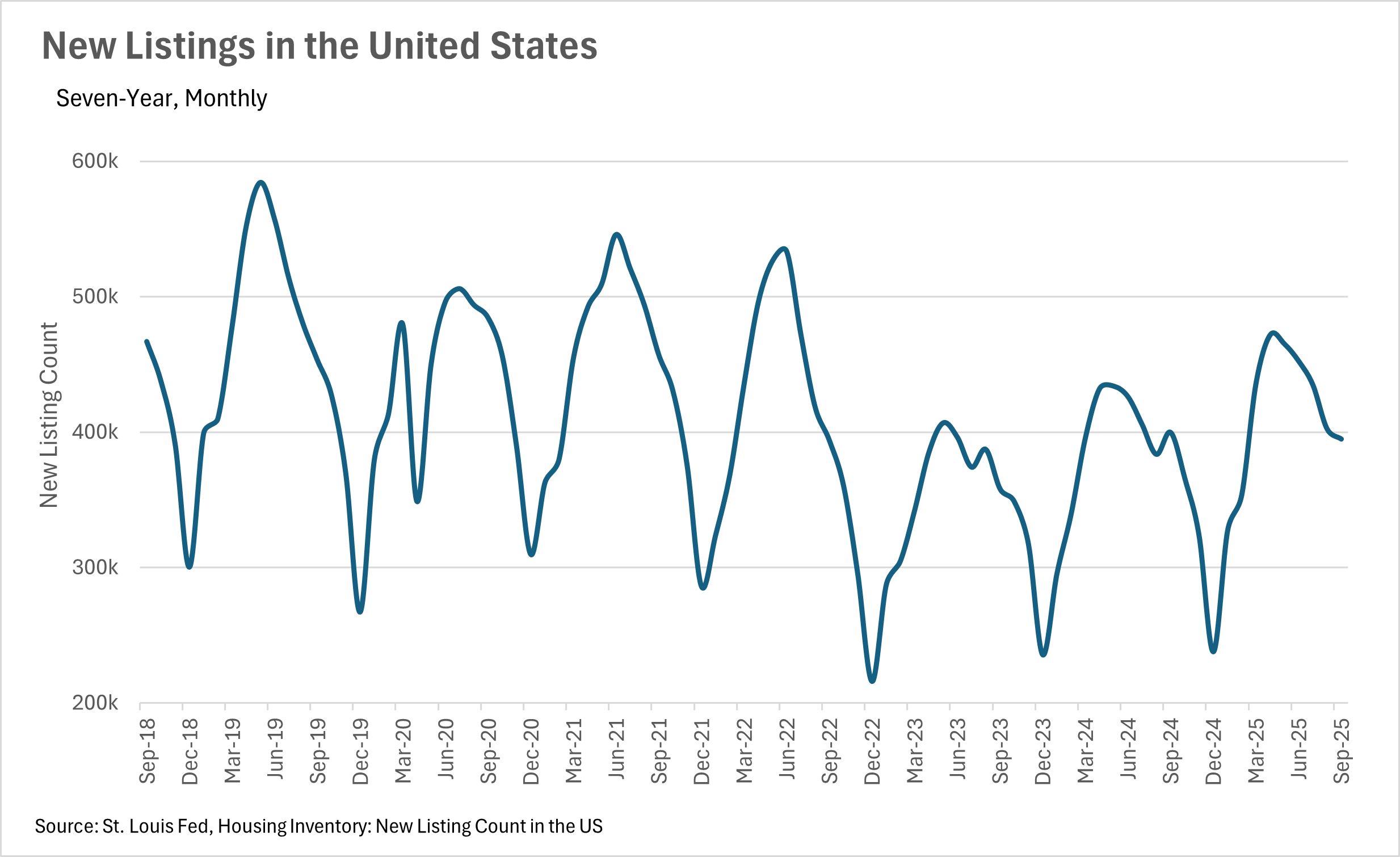

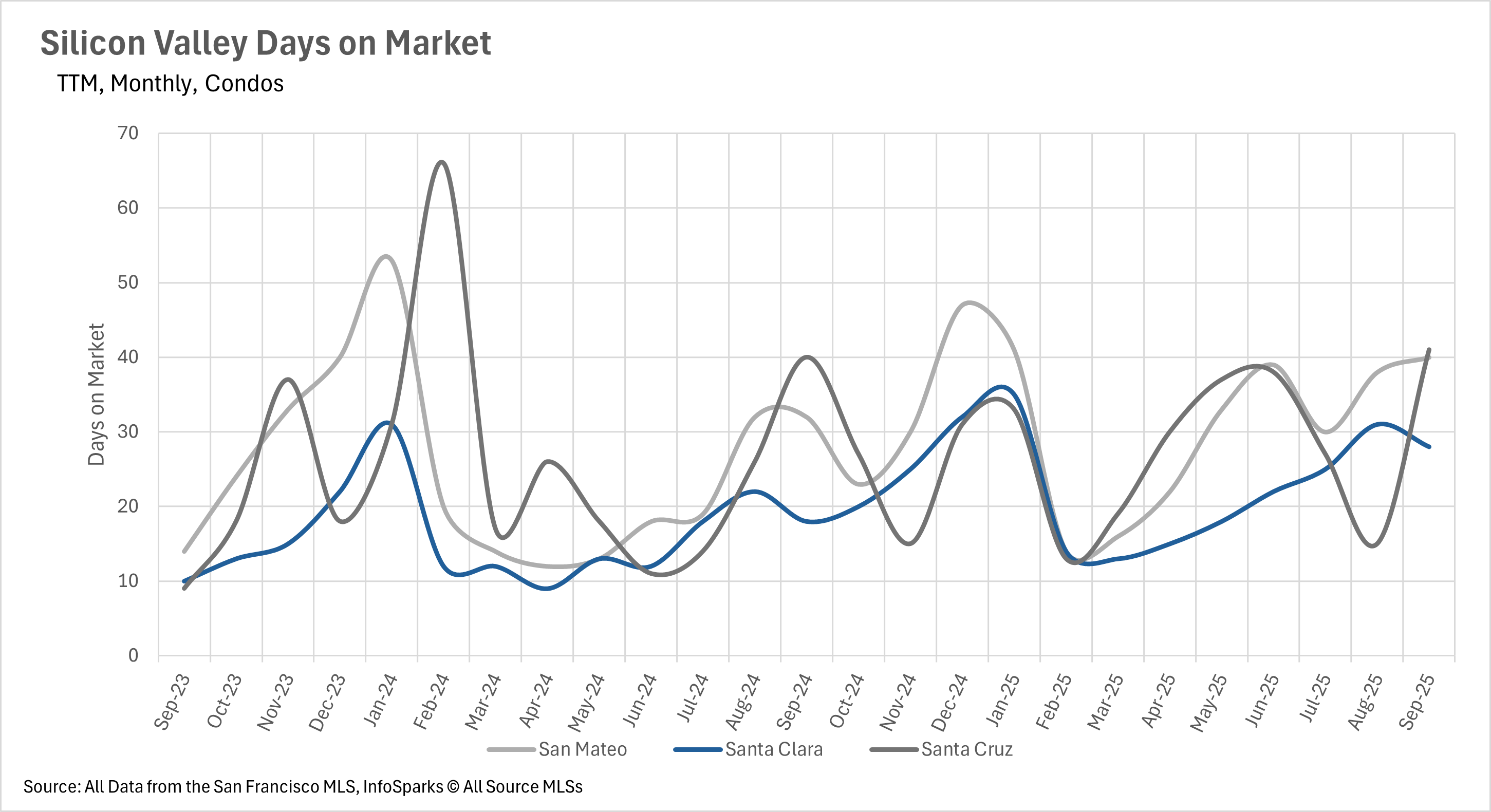

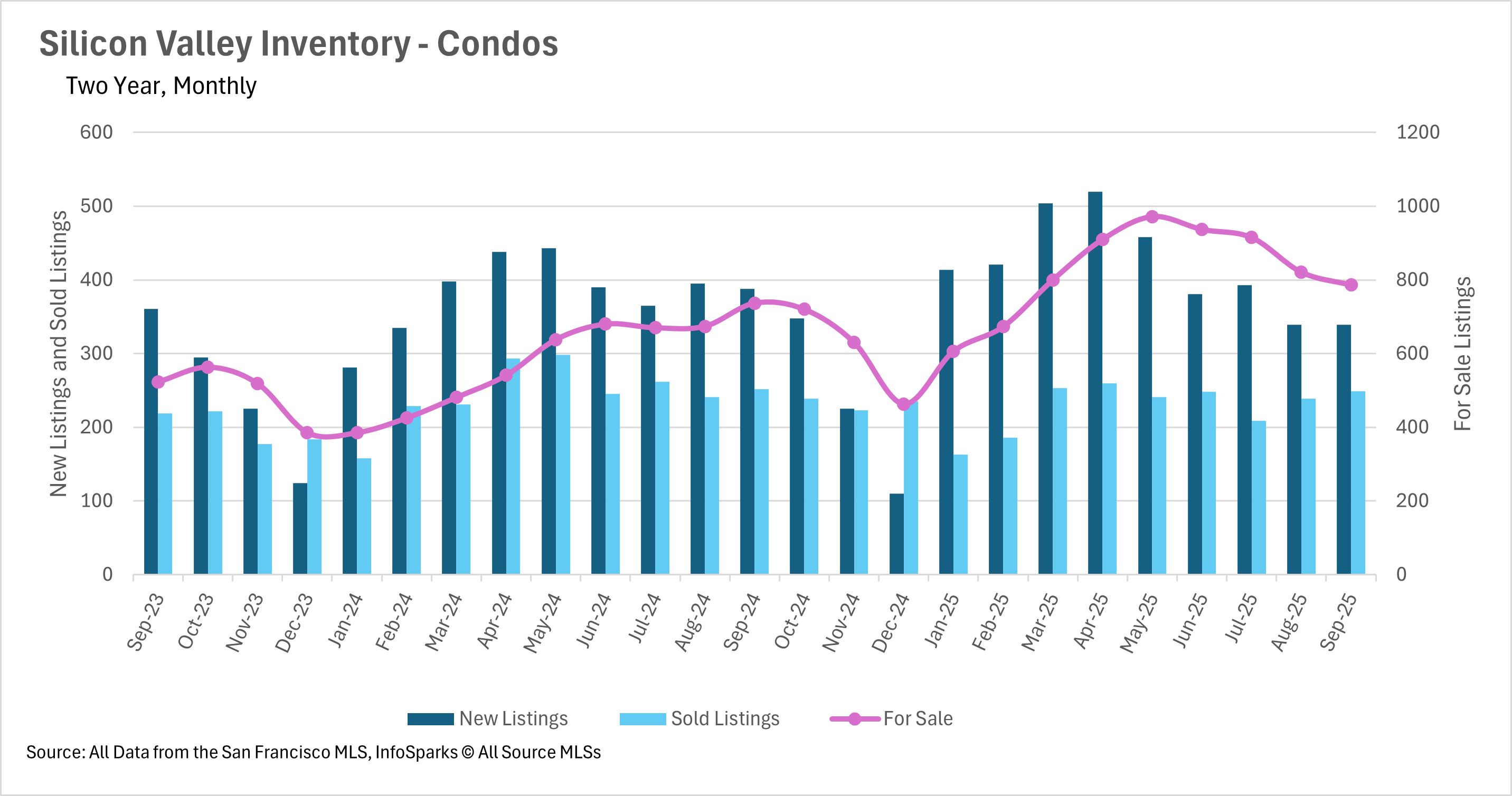

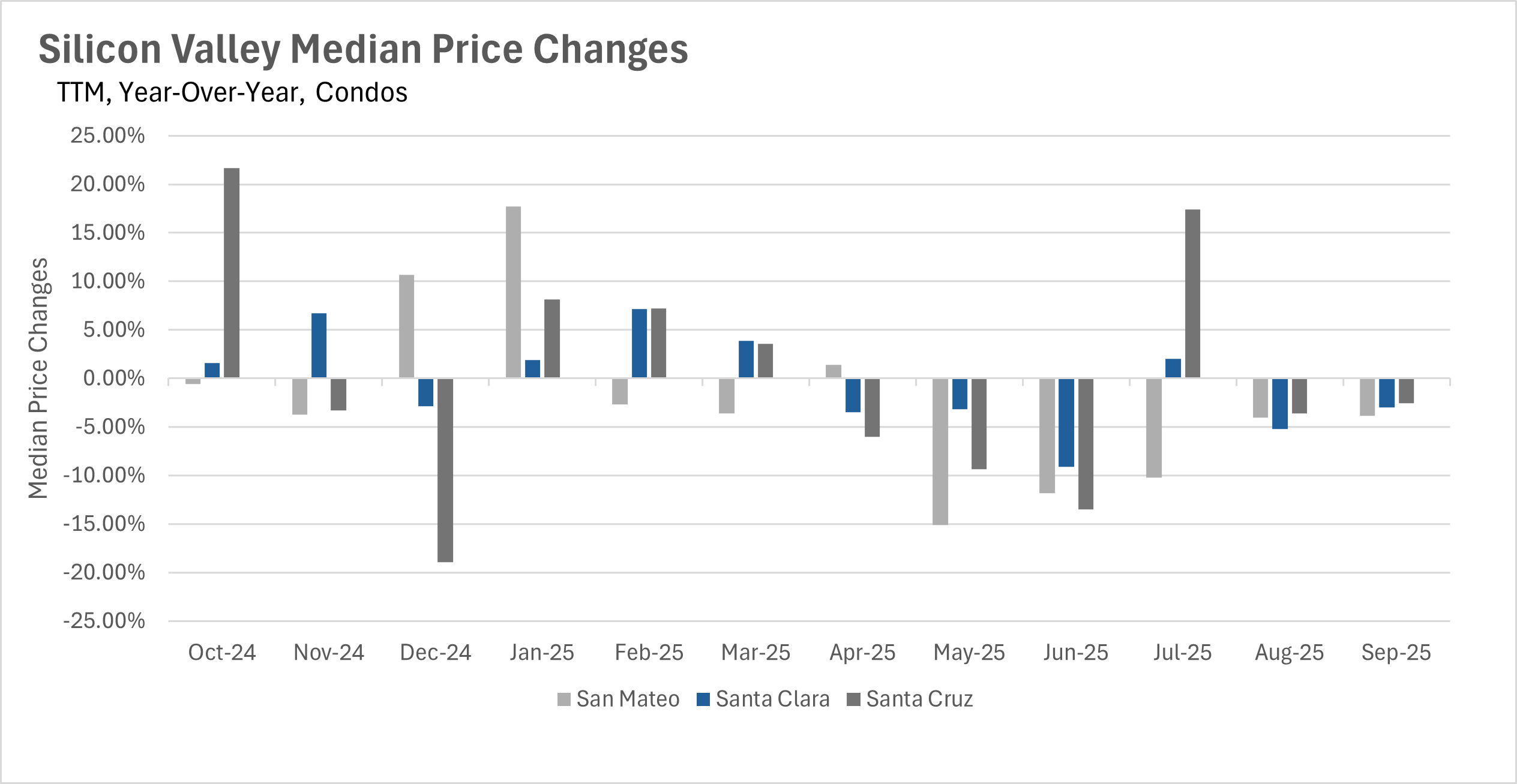

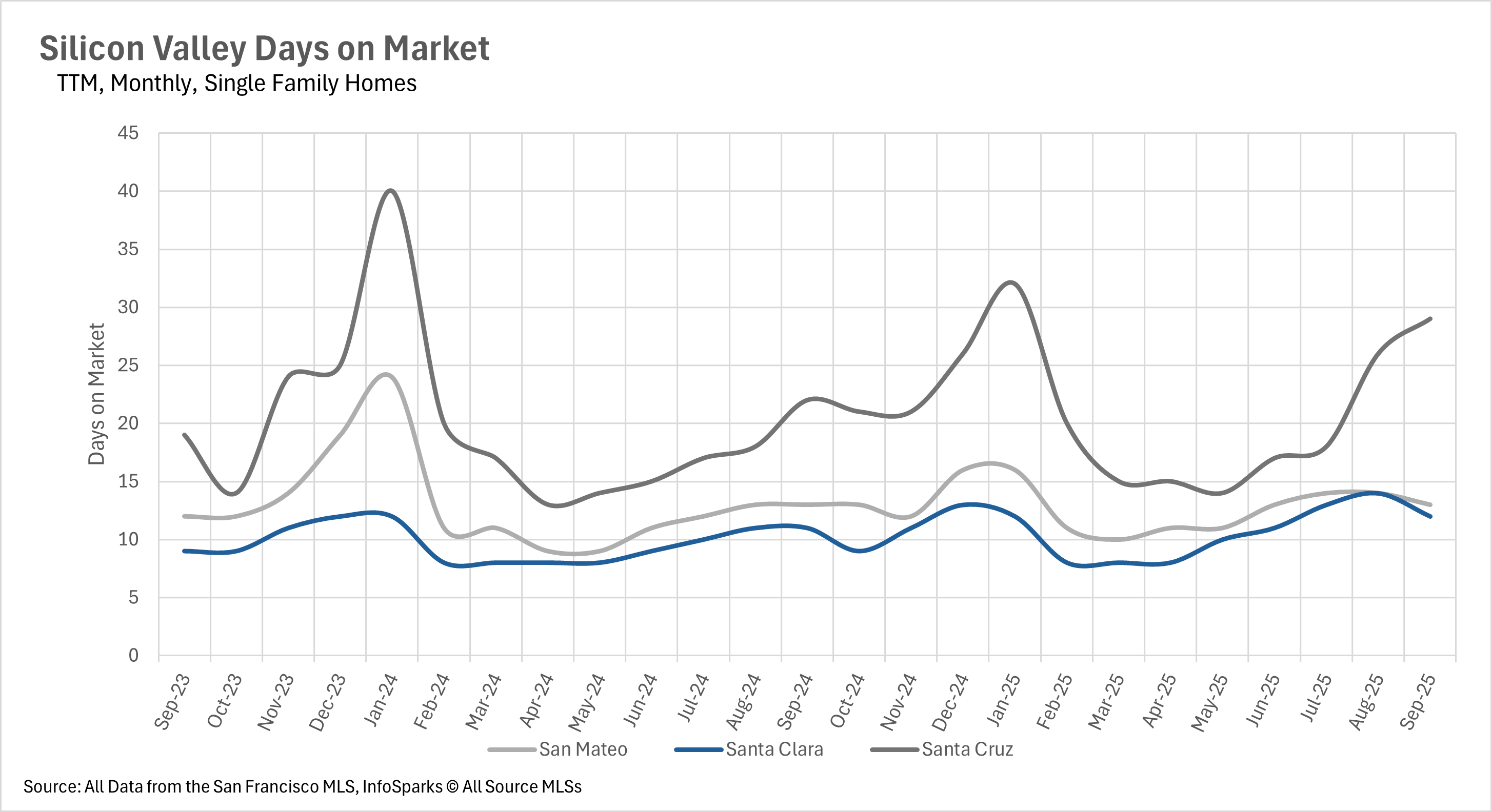

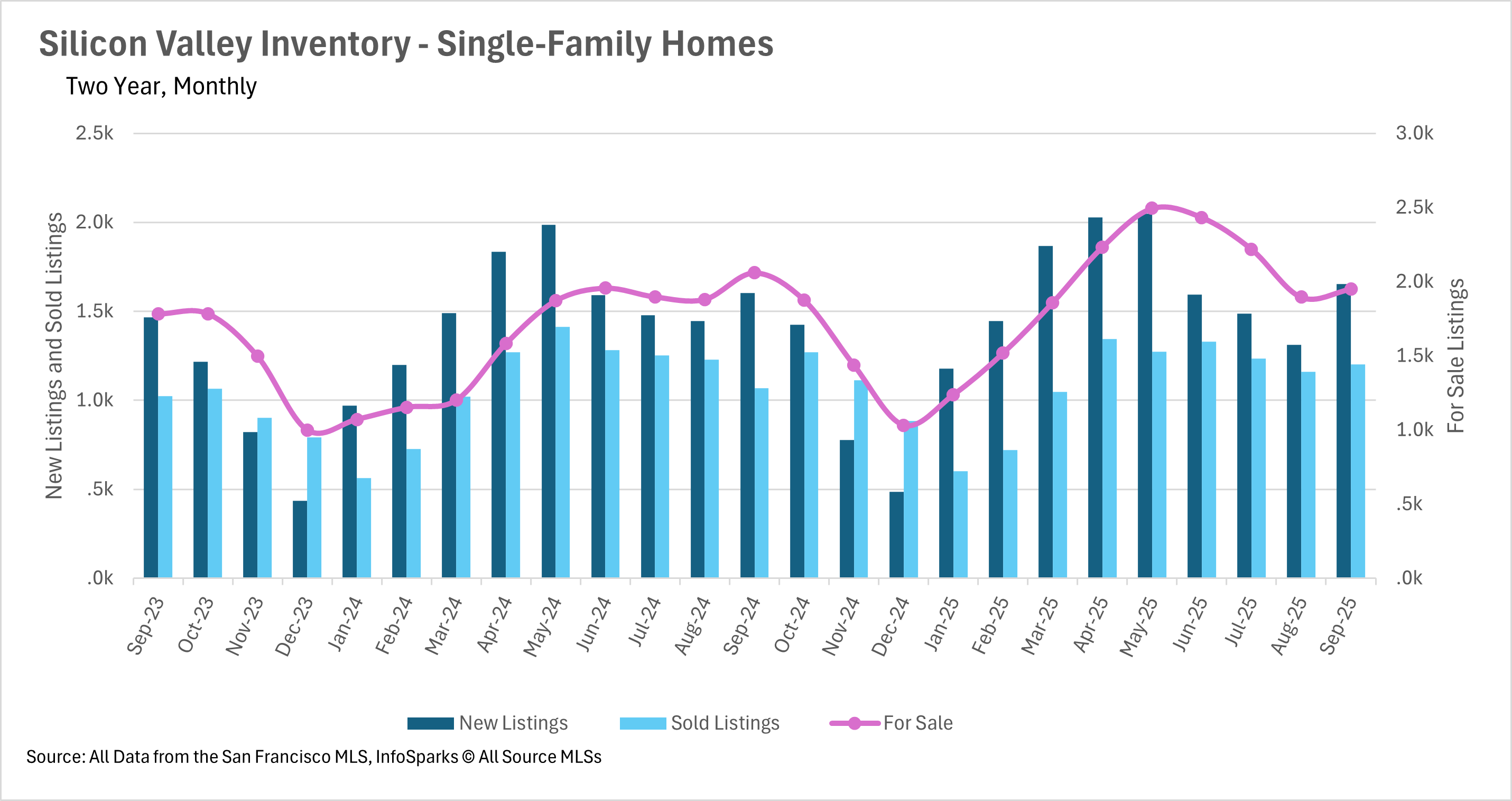

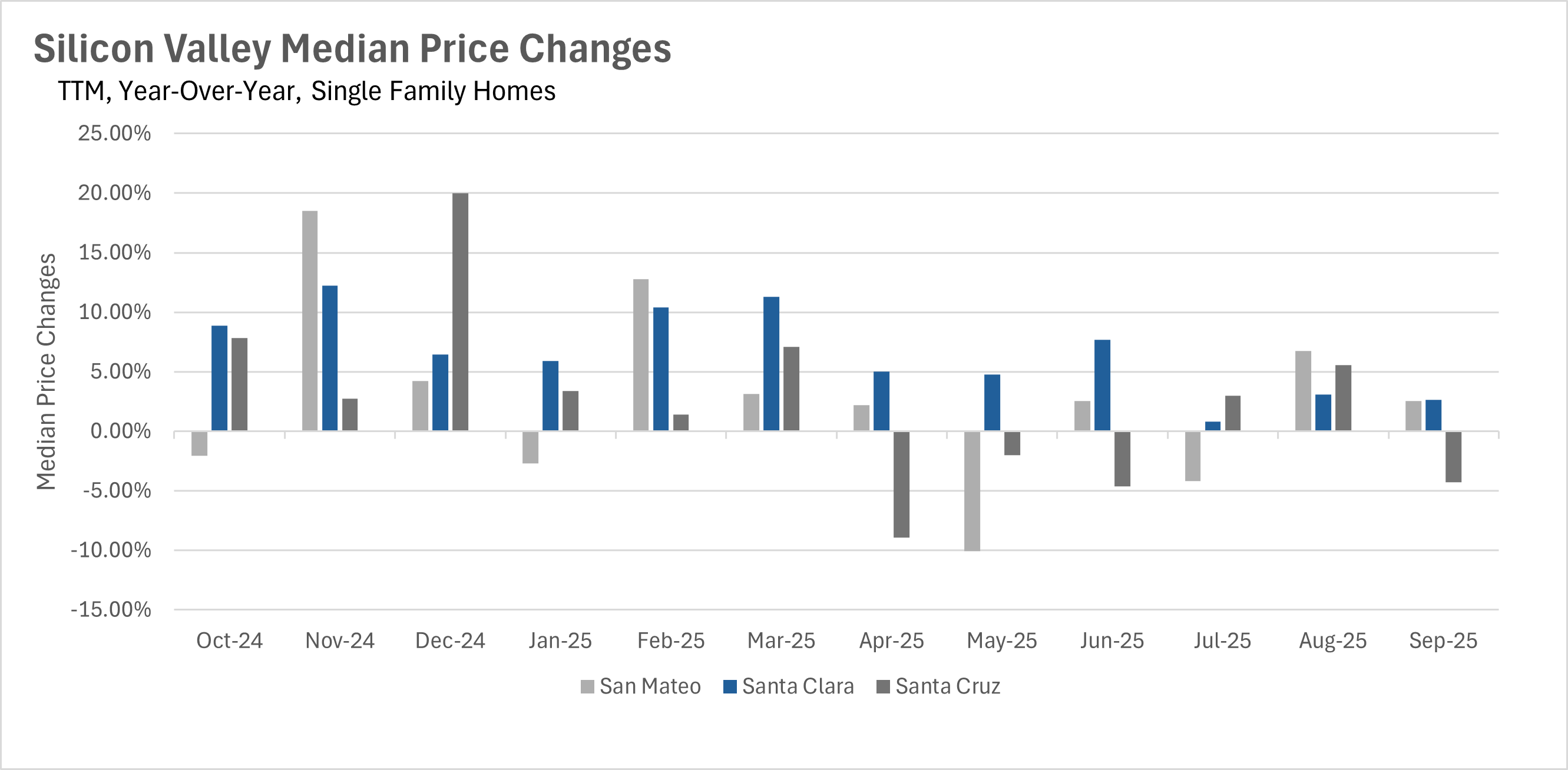

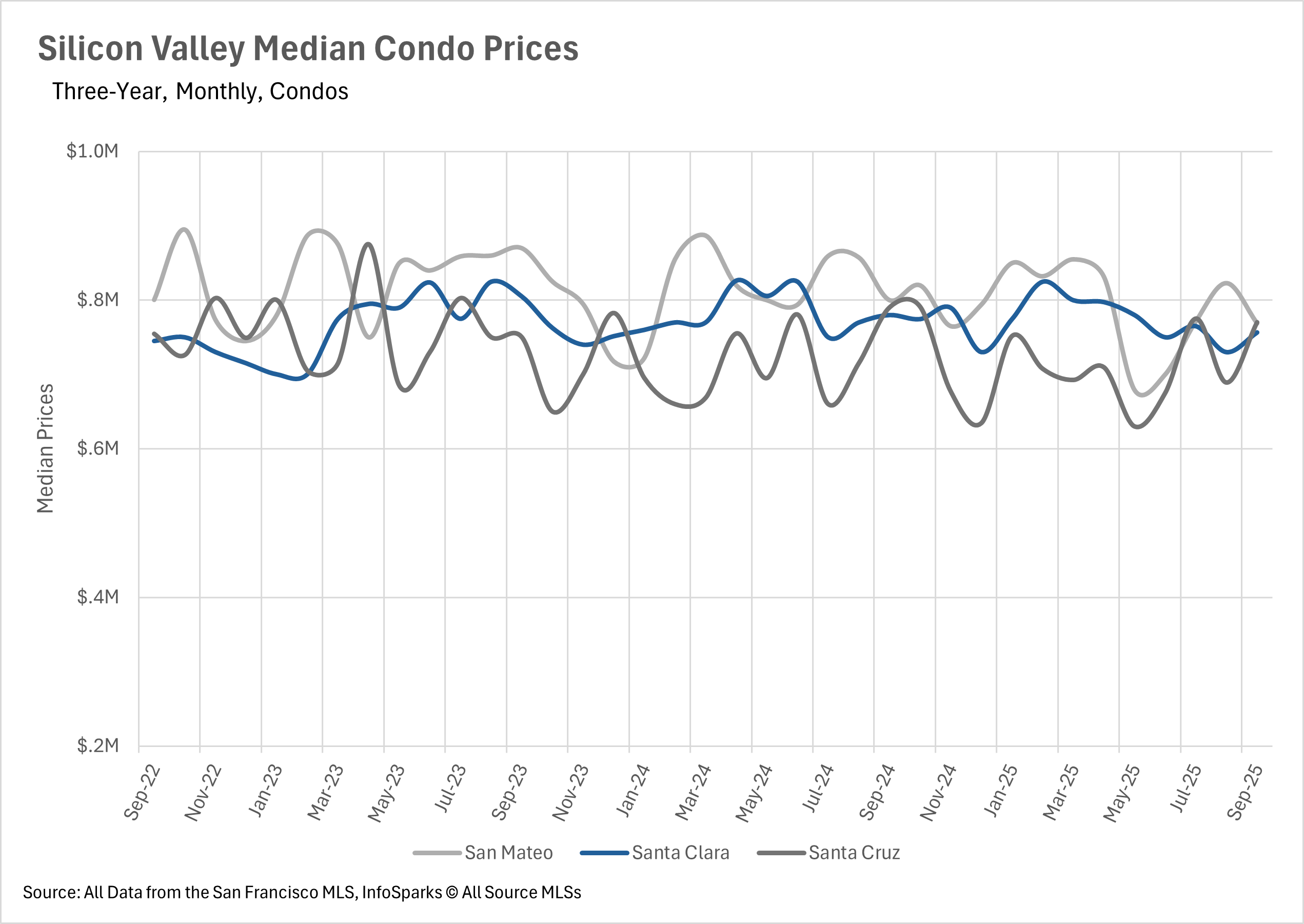

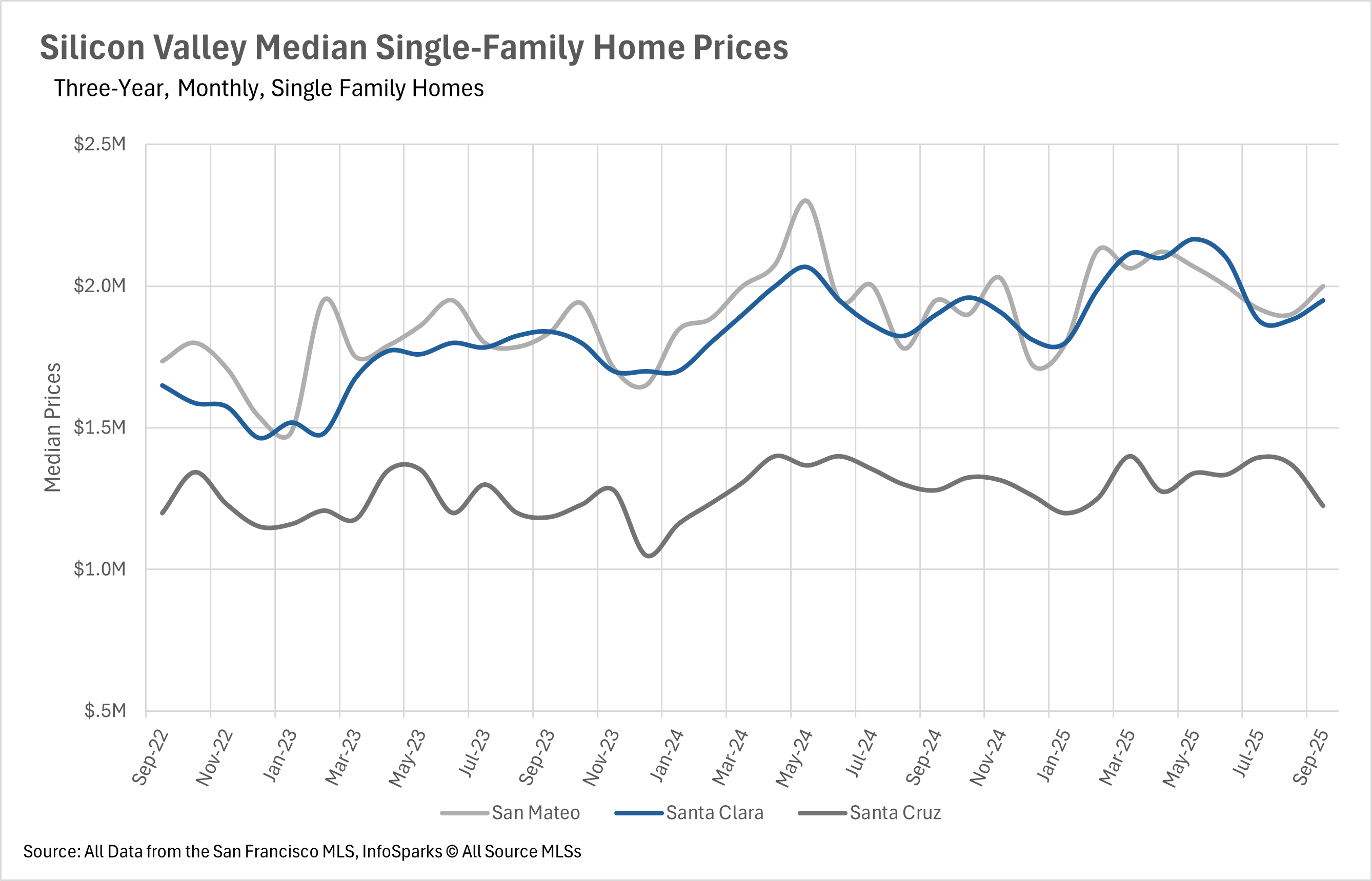

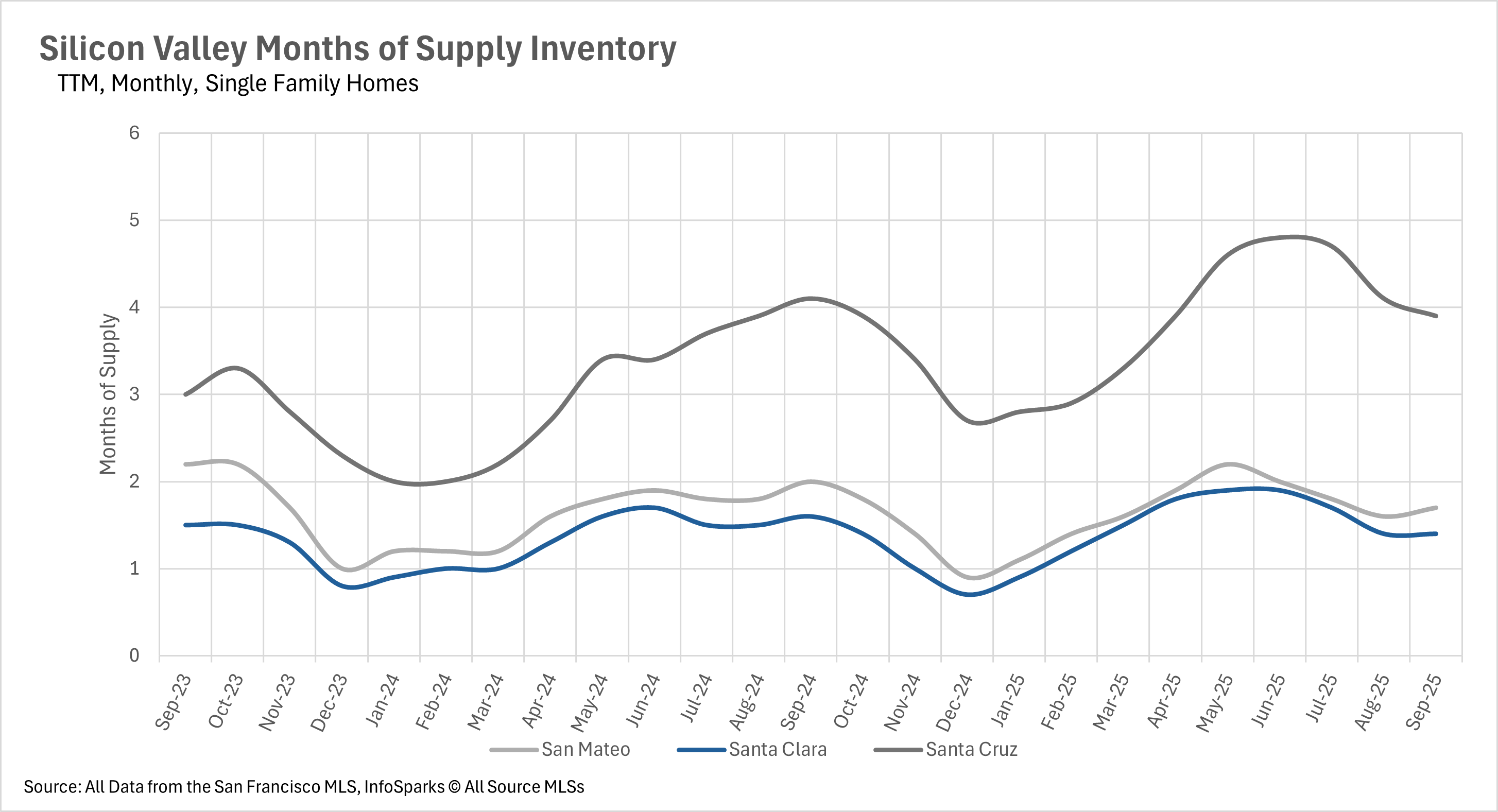

As we move into the seasonally slow months, the market environment that we’re in is setting up for what could be a very interesting 2026. Inventories are still growing (for now), and interest rates are falling, which could put us in a very interesting position when the spring frenzy begins next year. It’ll be important to keep a keen eye on both the market and broader macroeconomic conditions throughout the fall and winter, so that you and your clients are ready for whatever spring has to throw at you.

Patrice and the Illuminate Properties team specialize in helping Palo Alto, Mountain View, Los Altos, Los Altos Hills, Menlo Park, Portola Valley, Redwood City, San Carlos, Sunnyvale, and Woodside buyers and sellers navigate today’s evolving market with confidence.

Stay up to date on the latest real estate trends.

Discover the fascinating history of Menlo Park’s tech industry, from the invention of the computer mouse and the birth of personal computing to Sand Hill Road venture … Read more

Explore the May 2026 Silicon Valley housing market update. Learn how rising home prices, increasing inventory, lower mortgage rates, and strong buyer demand are shapin… Read more

Discover the best outdoor activities in Los Altos Hills, CA. Explore Hidden Villa, scenic hiking trails, bird watching, photography spots, picnicking, and nature exper… Read more

Planning a home remodel in Los Altos? Learn how to budget, hire contractors, manage permits, avoid delays, and create a stress-free renovation experience with this com… Read more

Buying a home in Menlo Park requires more than a strong offer — it requires strategy, preparation, and expert representation. This guide explains how buyers can compet… Read more

Preparing a Los Altos Hills estate for sale requires more than simple cosmetic updates. Today’s luxury buyers are paying close attention to property condition, wildfir… Read more

You’ve got questions and we can’t wait to answer them.