Silicon Valley Newsletter - November

Real Estate

Real Estate

Stay up to date on the latest real estate trends.

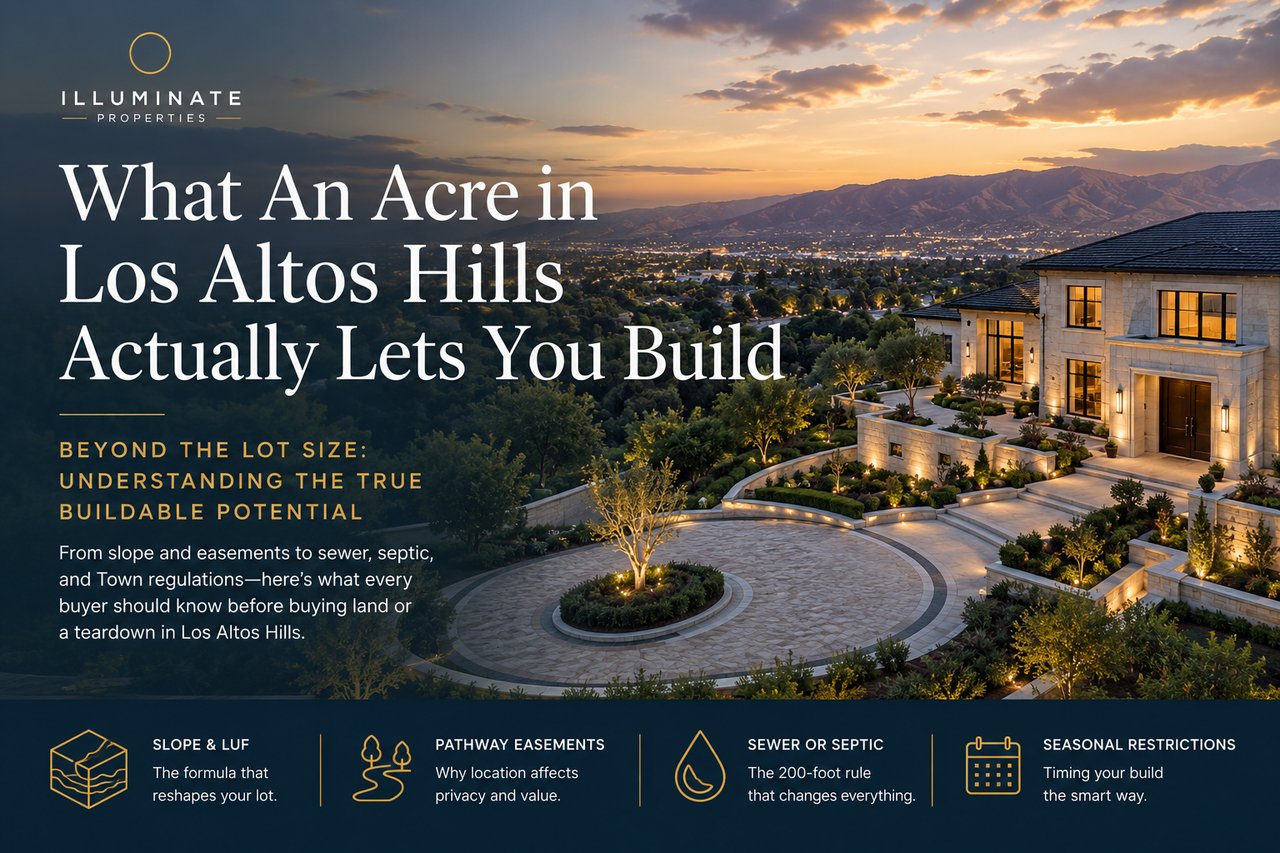

Learn what you can build on one acre in Los Altos Hills, including LUF, MDA, slope, septic, sewer, pathway easements, and key due diligence tips.

Explore the latest Silicon Valley real estate market update for June. Discover home prices, inventory, buyer demand, and housing trends across San Mateo, Santa Clara, … Read more

Planning to move to Mountain View? Discover the best neighborhoods, schools, parks, commuting options, and local lifestyle in this complete Mountain View relocation gu… Read more

Learn how water-smart landscaping can increase your Los Altos Hills home's value with drought-tolerant plants, smart irrigation, fire-wise design, and sustainable luxu… Read more

Discover how Sand Hill Road shapes Menlo Park home values. Learn how venture capital, luxury neighborhoods, buyer demand, and Silicon Valley drive real estate prices.

Explore the best outdoor activities in Menlo Park, CA. Discover parks, hiking trails, bike paths, swimming, golf, and recreation that make Menlo Park an ideal place to… Read more

You’ve got questions and we can’t wait to answer them.